Can You Reaffirm A Debt In Chapter 13

Can You Reaffirm A Debt In Chapter 13 - It is however very unlikely that if you continue to repay the note that the bank would foreclose anyway. Web you can reaffirm the debt(s) during the chapter 7 case, which means you accept the debt(s) as valid and promise to pay it/them, even though it/they could be discharged (eliminated) in bankruptcy. You usually have to formally reaffirm the debt. Web here are examples of the reaffirmation of a secured debt (like a vehicle loan) in a chapter 7 case vs. In both cases, you can surrender the collateral, which means the debt. As long as the codebtor stay is in effect, your creditors can… When you’re able to keep the collateral in chapter 7 if you are current on your debt payments, you would very likely be able to keep your collateral/vehicle under chapter 7. Web when you file for chapter 13, you'll have a choice for debt secured by collateral, such as your house, car, or other property: Web certain debts can not be discharged in a chapter 7 or a chapter 13 bankruptcy case. Web chapter 13 bankruptcy.

The last blog post was about when to reaffirm a secured debt under chapter 7 and when to handle that under chapter 13 instead. You are not required to reaffirm any debt or sign any agreement regarding a debt that has been or will be discharged in your bankruptcy case. Web you should have already paid off the mortgage arrears in your chapter 13 if it is complete and there is no need to reaffirm. Web here are examples of the reaffirmation of a secured debt (like a vehicle loan) in a chapter 7 case vs. These are assets that you cannot. Web chapter 13 bankruptcy. It is however very unlikely that if you continue to repay the note that the bank would foreclose anyway. As for the discharge, after you. The federal bankruptcy code states that if you do not reaffirm that the secured creditor can repossess even if you remain current with the payments. The lender and the court must be persuaded to approve your reaffirmation.

The lender and the court must be persuaded to approve your reaffirmation. That means you exclude that debt from the discharge (legal write off) that chapter. In both cases, you can surrender the collateral, which means the debt. Web when you file for chapter 13, you'll have a choice for debt secured by collateral, such as your house, car, or other property: When you sign a reaffirmation agreement, you assume liability for a debt that would otherwise be eradicated in your bankruptcy. Web reaffirming your mortgage creates new debt: With a chapter 7 bankruptcy, the trustee gathers and liquidates your nonexempt assets. Addressing it in a chapter 13 case. Keep the secured property and continue paying the monthly amount, plus arrearages, in your repayment plan, or. Web chapter 13 bankruptcy.

Bankruptcy FAQs Sagre Law Firm

Web certain debts can not be discharged in a chapter 7 or a chapter 13 bankruptcy case. The last blog post was about when to reaffirm a secured debt under chapter 7 and when to handle that under chapter 13 instead. When you sign a reaffirmation agreement, you assume liability for a debt that would otherwise be eradicated in your.

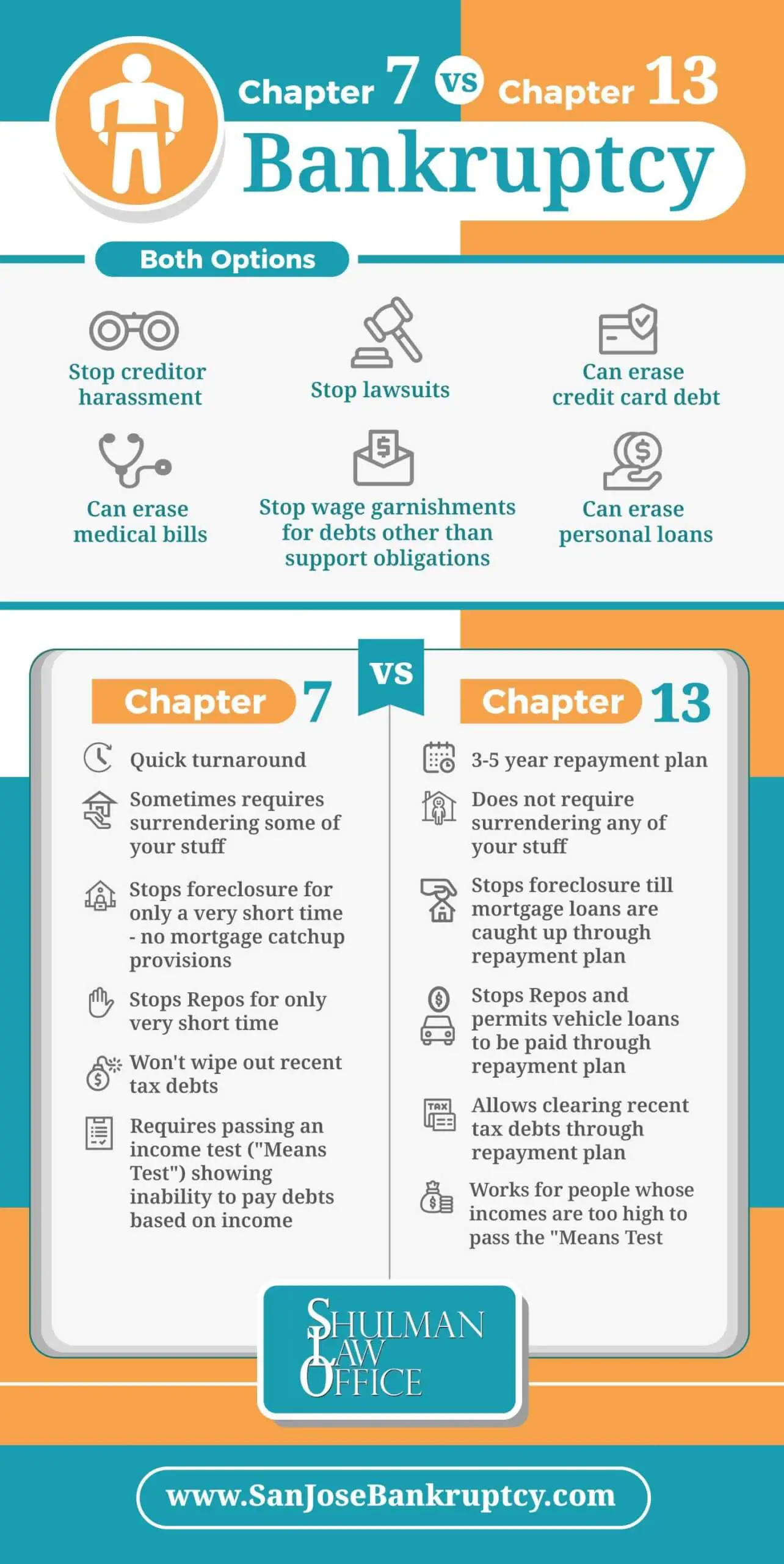

Infographic Chapter 7 vs. Chapter 13 BankruptcyWeaver Bankruptcy Law Firm

In both cases, you can surrender the collateral, which means the debt. Web certain debts can not be discharged in a chapter 7 or a chapter 13 bankruptcy case. Those who want to keep their mortgage or other secured debt as is during a chapter 13 bankruptcy filing will need to reaffirm the account during their bankruptcy proceeding, essentially agreeing.

Neil T Anderson Quote “The more you reaffirm who you are in Christ

Addressing it in a chapter 13 case. Web you should have already paid off the mortgage arrears in your chapter 13 if it is complete and there is no need to reaffirm. At the end of your repayment period, any remaining debt is discharged. Web you are not required to sig a reaffirmation agreement. The amount of equity you have.

What Happens After You File Bankruptcy

Web you can reaffirm the debt(s) during the chapter 7 case, which means you accept the debt(s) as valid and promise to pay it/them, even though it/they could be discharged (eliminated) in bankruptcy. When you’re able to keep the collateral in chapter 7 if you are current on your debt payments, you would very likely be able to keep your.

All About Reaffirmation Agreements in Bankruptcy

The federal bankruptcy code states that if you do not reaffirm that the secured creditor can repossess even if you remain current with the payments. It is however very unlikely that if you continue to repay the note that the bank would foreclose anyway. Web certain debts can not be discharged in a chapter 7 or a chapter 13 bankruptcy.

Bankruptcy 101 LoanPro Help

As long as the codebtor stay is in effect, your creditors can… With this type of bankruptcy, you can keep your property as long as you. Web but since secured debts are connected to collateral, you don't get to keep the collateral unless you pay the debt. Keep the secured property and continue paying the monthly amount, plus arrearages, in.

6 Things You Can Reaffirm for Positive Change and Validation

The amount of equity you have in the property is also essential. The lender and the court must be persuaded to approve your reaffirmation. You may lose the property if you can… You usually have to formally reaffirm the debt. Web but since secured debts are connected to collateral, you don't get to keep the collateral unless you pay the.

SHOULD I REAFFIRM MY MORTGAGE AGREEMENT AFTER MY CHAPTER 7 BANKRUPTCY?

In chapter 13, you repay secured debts through the repayment plan. These are assets that you cannot. Web here are examples of the reaffirmation of a secured debt (like a vehicle loan) in a chapter 7 case vs. Web chapter 13 bankruptcy. If you want to refinance to get a lower interest rate it should be no problem.

What Is The Difference In Chapter 7 And 13 Bankruptcy

The amount of equity you have in the property is also essential. Web certain debts can not be discharged in a chapter 7 or a chapter 13 bankruptcy case. In both cases, you can surrender the collateral, which means the debt. The lender and the court must be persuaded to approve your reaffirmation. At the end of your repayment period,.

Reaffirming Debts After Chapter 7 Bankruptcy By Petitioners

That means you exclude that debt from the discharge (legal write off) that chapter. Keep the secured property and continue paying the monthly amount, plus arrearages, in your repayment plan, or. Web but since secured debts are connected to collateral, you don't get to keep the collateral unless you pay the debt. Web you should have already paid off the.

The Lender And The Court Must Be Persuaded To Approve Your Reaffirmation.

When you’re able to keep the collateral in chapter 7 if you are current on your debt payments, you would very likely be able to keep your collateral/vehicle under chapter 7. Web chapter 13 bankruptcy. Those who want to keep their mortgage or other secured debt as is during a chapter 13 bankruptcy filing will need to reaffirm the account during their bankruptcy proceeding, essentially agreeing to continue paying on the debt. In chapter 13, you repay secured debts through the repayment plan.

In Both Cases, You Can Surrender The Collateral, Which Means The Debt.

Web you will need to reaffirm or renegotiate your mortgage. With a chapter 7 bankruptcy, the trustee gathers and liquidates your nonexempt assets. This means that you will be responsible for paying the mortgage, even if the value of your home has decreased. It is however very unlikely that if you continue to repay the note that the bank would foreclose anyway.

You Usually Have To Formally Reaffirm The Debt.

Web when you file for chapter 13, you'll have a choice for debt secured by collateral, such as your house, car, or other property: Web reaffirming your mortgage creates new debt: Web you can reaffirm the debt(s) during the chapter 7 case, which means you accept the debt(s) as valid and promise to pay it/them, even though it/they could be discharged (eliminated) in bankruptcy. As for the discharge, after you.

Keep The Secured Property And Continue Paying The Monthly Amount, Plus Arrearages, In Your Repayment Plan, Or.

That means you exclude that debt from the discharge (legal write off) that chapter. At the end of your repayment period, any remaining debt is discharged. This kind of comparison of options can. Web but since secured debts are connected to collateral, you don't get to keep the collateral unless you pay the debt.